Your monthly subsidy depends on whether you are enrolled in Medicare:

If you are (1) under age 65 and not enrolled in Medicare or, (2) at least age 65 and enrolled in Medicare Part B only, monthly subsidy maximums are calculated as follows:

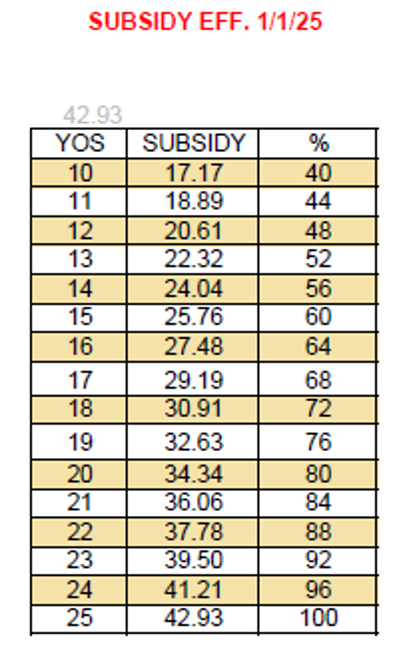

- Formula: The retiree’s Years of Service (YOS) x 4% x Maximum Subsidy Amount* = Monthly Subsidy

UNFROZEN SUBSIDY: If the retiree either (1) entered DROP or retired prior to July 15, 2011 or (2) chose to opt in during the designated period, the qualified survivor is entitled to the updated monthly subsidy maximum effective January 1st.

- If for example, the retiree had 20 years of service and the maximum subsidy was $939.09, then the amount of subsidy you will receive toward your health insurance premium is $751.27 (20 YOS x 4% x $939.09 = $751.27).

*The Maximum Subsidy Amount is based on the retiree’s DROP entry or retirement date.

Amounts shown above are for illustration purposes only. Please click here to view the current subsidy.

FROZEN SUBSIDY: If the retiree either entered DROP or retired on July 15, 2011 or later and chose not to opt in during the designated period, the qualified survivor is entitled to a monthly subsidy maximum of $595.60, the rate effective July 1, 2011.

If you are enrolled in Medicare Parts A and B, subsidy formulas are plan-specific and you are reimbursed the basic Part B premium. At age 65, if you do not qualify for Medicare Part A (all pensioners will qualify for Medicare Part B), the above formula will be used to calculate your subsidy amount and, additionally, you will not be reimbursed the basic Part B premium. If you are enrolled in Medicare Parts A and B, the following monthly subsidy maximums are as follows:

UNFROZEN SUBSIDY: If the retiree either (1) entered DROP or retired prior to July 15, 2011 or (2) chose to opt in during the designated period, the qualified survivor is subject to the updated monthly subsidy maximum effective January 1st.

Click here to view the current subsidy.

FROZEN SUBSIDY: If the retiree did not choose to opt in during the designated period and entered DROP or retired on July 15, 2011 and later, the qualified survivor is frozen at the monthly subsidy maximum of $480.41, the rate effective July 1, 2011.

*If the retiree had 20 to 25 years of service, the qualified survivor is eligible for 100% of the monthly subsidy maximum as stated. If the retiree had 15 to 19 years of service, the qualified survivor is eligible for 90% of the monthly subsidy maximum as stated. If the retiree had 10 to 14 years of service, the qualified survivor is eligible for 75% of the monthly subsidy maximum as stated.

While you may cover dependents under your plan, please note that the subsidy may only be applied to the cost of the single-party coverage. If the single-party plan premium is higher than your eligible subsidy, the difference (including the premium for dependent coverage, if applicable) will be taken in the form of a deduction on your monthly pension payment. If your eligible subsidy exceeds the single-party plan premium, the unapplied subsidy amount is forfeited and any premium for dependent coverage will be taken in the form of a deduction on your monthly pension payment.

California State Income Tax Withholding Form

California State Income Tax Withholding Form Federal Income Tax Withholding Form

Federal Income Tax Withholding Form